Presented by: Johnathon Opet, CFP®

You’ve put in the hard work of saving for college, and now it’s time to start using those 529 plan assets to help with a family member’s education-related costs. But before you begin withdrawing those funds, it’s important to understand the difference between qualified and nonqualified expenses.

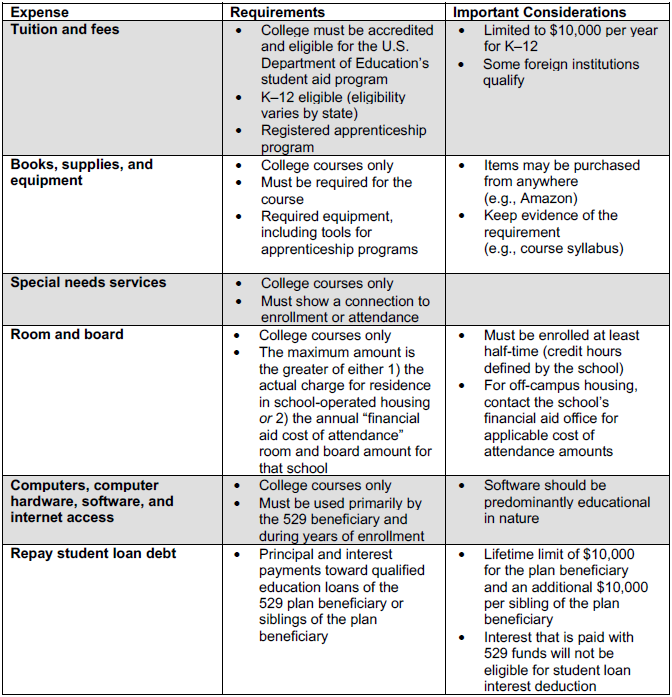

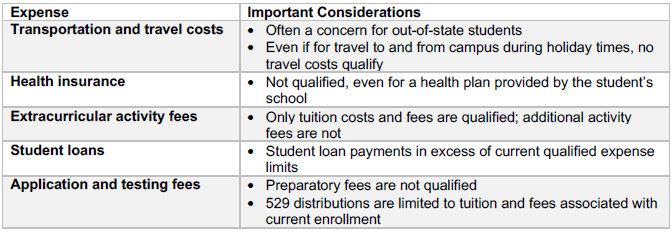

The charts below provide an overview of some of the most common qualified and nonqualified expenses.

Qualified Expenses

Nonqualified Expenses

Please note: Just because an expense is nonqualified, it doesn’t mean the 529 plan funds cannot be considered a source of payment. The main consequence of paying nonqualified expenses from the 529 plan is that the gains portion of that distribution will be taxed, and it could be assessed a 10 percent penalty.

For more information on 529 plans (referred to as “Qualified Tuition Programs”) and for examples of tax and coordination calculations, see the Qualified Tuition Programs section of IRS Publication 970.

Questions?

Contact us! We’re happy to help.

This material has been provided for general informational purposes only and does not constitute either tax or legal advice. Although we go to great lengths to make sure our information is accurate and useful, we recommend you consult a tax preparer, professional tax advisor, or lawyer.

Johnathon Opet, CFP® is a financial advisor located at EmVision Capital Advisors, 251 W. Garfield Rd. Suite 155 Aurora, OH 44202. He offers securities and advisory services as an Investment Adviser Representative of Commonwealth Financial Network®, Member FINRA/SIPC, a Registered Investment Adviser. He can be reached at (330)954-3770 or at info@emvisioncapital.com.

©2022 Commonwealth Financial Network®